As the number of Americans without any health insurance continues

to rise and health-insurance premiums escalate, once again, at double-digit

annual increases, health policy is bound to move once more to the

center of the domestic policy debate. It is a propitious time to

take stock of the nation’s health system and to explore the

options before the nation.

A. An International Perspective

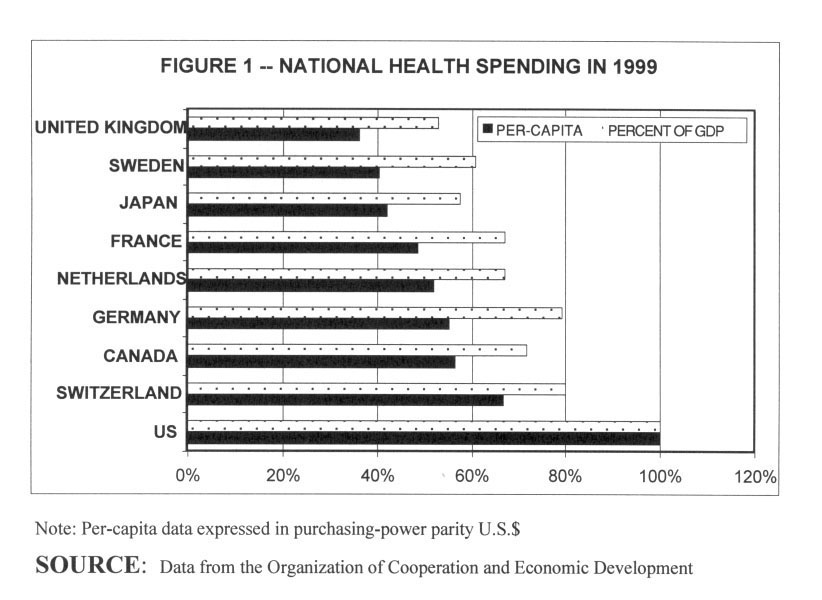

The United States has long been the most expensive health system

in the world, and it remains so today, even after a decade of "managed

care." Table 1 shows the most recent available data on total

national health spending in 1999, with the U.S. per-capita health

spending ($4,358) and U.S. percentage of GDP spent on health care

(13%) each set to 100%. The ranking for 1990 would have been quite

similar. Several points may be noted in connection with this table.

Table 1- per capita

spending and percent of GDP

Note: Per-capita data expressed in purchasing-power

parity U.S.$

SOURCE: Data from the Organization of Cooperation and Economic

Development

First, with the exception of Canada, the populations of all other

nations shown in the graph are much older than ours. To illustrate,

only in the year 2020 will the percentage of the American population

over age 65 reach the current German percentage, and only in 2025

will the American age structure reach Sweden’s current age structure.

Second, if one distinguishes between real health care services (physician

visits, hospital days, drugs, supplies, and so on) and financial resources

(spending), it is found that most of the nations shown in Table 1

actually devote more real resources overall per capita to health care

than does the U.S. The U.S. does rank higher, however, in the availability

and use of highly sophisticated medical technology.

Third, as is seen in Table 1, all other industrialized nations cede

to the providers of health care (doctors, nurses, pharmaceutical manufacturers,

etc.) a much smaller fraction of the nation’s GDP than does the

U.S. The other nations can do this because the structure of their

health insurance systems amasses monopsonistic (single-buyer) market

power on the demand side of the market , which allows third-party

payers to pay the providers of health care lower money prices for

that care than they would have to pay under the more loosely structured

U.S. system. It is the reason, for example, why prices for the same

brand-name prescription drugs can be so much higher in the U.S. than

in Canada and Europe, and why American physicians are much better

paid than their colleagues abroad. On average, the net income of American

physicians in 1999 was 5.5 times average employee compensation. The

comparable numbers for Germany and Canada are 3.4and 3.2, respectively.

Fourth, the U.S. has by far the most complex and bureaucratic health-insurance

system in the world. In an elaborate cross-national study of health

spending in 1990 published in 1996, for example, the McKinsey Global

Institute found that after all conceivable adjustments were made for

demographic and other differences between nations, Germans in 1990

spent an average $390 more on health care proper than did Americans,

while Americans spend $360 more on "administration" and

another $256 more on "other" items not specifically identified

by McKinsey, but probably including still other administrative overhead.

There simply does not exist anywhere in the world a pluralistic health

insurance system as complex, as paper hungry and as computer- and

labor-intensive as is the American system.

Fifth, on most measurable, population-based health status indicators

— e.g., life expectancy at birth or at age 65, infant mortality,

preventable years of life lost — the U.S. always has ranked and

continues to rank rather poorly relative to the rest of the industrialized

world. Neighboring Canada, whose age structure is similar to ours,

and which spends less than 60% of the comparable U.S. figure on health

care per capita, ranks higher than the U.S. on all of these indicators.

In fairness to the U.S. health system, however, it must be said that

these aggregate health status indicators are apt to reflect mainly

socio-economic influences beyond the control of the health sector

proper. Unfortunately, there is very little solid information on what

added benefits in terms of health status or personal comfort the U.S.

actually is buying with its much higher health spending. Curiously,

American policy makers and research foundations never have shown much

interest in this intriguing question. The well-endowed Robert Wood

Johnson Foundation, for example, declines to fund such research as

a matter of explicit policy.

Well-insured Americans

It probably is fair to say, on the basis of impressionistic information,

that well-insured Americans with complex diseases tend to find in

the U.S. health system more aggressive, highly sophisticated diagnoses

and medical treatments — or have speedier access to such treatments

— than might similar patients in other nations. It is one reason

why health care of this sort has become an American export that serves

a global market.

Low-income families

On the other hand, low-income families without health insurance probably

fare worse in the U.S. health system than they would in other nations.

At this time, more than 40 million mainly low-income Americans (about

7 million children among them) do not have health insurance of any

sort, a number that rose from about 35 million in 1990, as America

prospered. More than two-thirds of the uninsured are low-income, most

are members of working families, and about half have been uninsured

for two years or more.

The elderly

Between 12 to 15 million elderly Americans do not have any insurance

coverage for prescription drugs.

The uninsured

While uninsured Americans usually do receive health care for truly

critical conditions, either with their own funds or on a charity

basis, it is well known to researchers that this care is not timely

and that lack of earlier intervention can have serious consequences

for the patient (see, for example, the Kaiser Family Foundation

website www.kff.org).

Bankruptcy

Furthermore, recent research conduced by Elizabeth Warren of the

Harvard Law School suggests that medical bills are the second most

frequently cited reasons for personal bankruptcy in the U.S., right

after loss of job and ahead of divorce. Citizens in other industrialized

nations would consider it morally unacceptable to let a family stricken

by major illness go bankrupt over the medical bills.

Ethic of health care

The chronic and growing presence of the uninsured in the U.S. and

their fiscal plight suggests that different nations posit different

ethical goals for their health systems. Canadians view comprehensive

health care as a social good that should be collectively financed

and made available to all citizens on equal terms. The entire Canadians

health system is structured to serve this explicitly articulated

social ethic. By contrast, Americans have never agreed on a distributive

ethic for their health system. While some Americans do subscribe

to a purely egalitarian ethic for health care practiced in Canada,

the politically dominant, policy-making elite in the U.S. has been

content to treat health-insurance and health care as basically a

private consumption goods whose content and quality can be allowed

to vary with the individual’s income.

As every first-year student in economics is taught — or should

be taught — it is impossible to compare public policies in

terms of their relative efficiency, if those policies aim at different

social goals. Therefore, it is not meaningful to ask which nation

— e.g., Canada or the U.S. — has the "best"

health system, because the two nations posit for their systems such

vastly different social ethics. It is all a matter of taste, and,

as the Romans so aptly put it, de gustibus non est disputandum.

B. The Wondrous Roller-Coaster Ride of U.S. Health Policy

Table 2 depicts the share of health spending paid by four groups

of payers: government, private insurance, other private third-party

payer and patients, out of pocket. Some remarkable features stand

out from the display. First, the share of health spending paid out

of pocket by patients has decreased steadily over time, although

it has remained stable since 1995. Out-of-pocket spending varies,

of course, enormously among families. Second, private insurance

now covers only a third of all health spending in the U.S., over

90% of it provided by employers at the place of work. Finally, governments

at all levels combined now represent the major source of all health

spending in the U.S. If one adds to the direct government payments

shown in Table 2 the roughly $130 billion or so added taxes all

taxpayers must pay annually to cover tax-revenues lost under the

tax-preference accorded employer-paid health insurance premiums

(these premiums are not added to the employee’s taxable income),

then more than 60% of all U.S. health spending is now tax-financed.

As a percentage of GDP, tax-financed health care in the U.S. now

exceeds tax-financed health care even in the U.K., with its government-run

health system.

Table 2

- sources of U.S. health spending 1965-2000

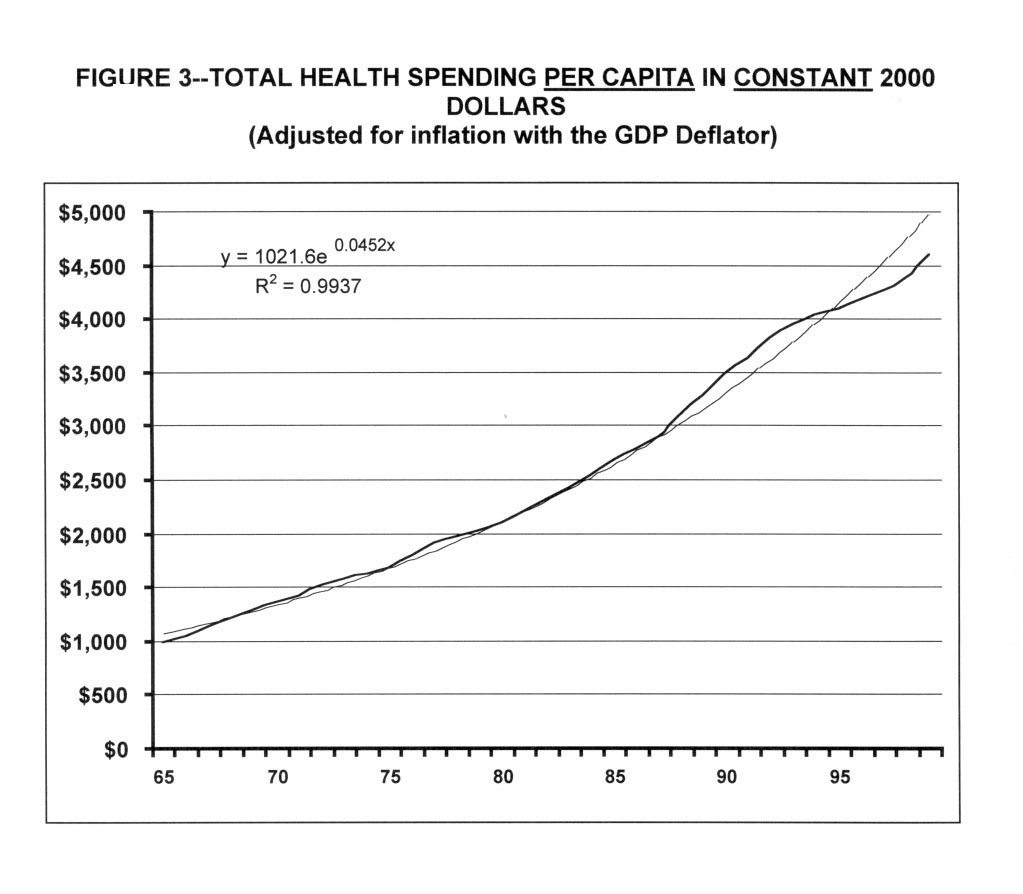

Table 2 shows the time path of per-capita U.S. health spending,

in constant (inflation-adjusted) dollars. It is seen that, from

1965 to about 1987, actual per-capita spending closely followed

a trend line according to which the health sector asked and received

from society, each year, 4.5% more real purchasing power per man,

woman and child than it did before. By contrast, constant-dollar

GDP per capita rose at a long-run average of only 1.7% per year

over the same period.

Table 3 - Total health spending per

capita in constant 2000 dollars (adjusted for inflation with

the GDP deflator)

Note: Per-captia data expressed in purchasing-power pariety

U.S. $

Source: Data from the Organization of Cooperation and Economic

Development

From 1987 on, actual spending rose above the historic trend line.

Most of the more rapid growth in spending originated in the private

insurance sector, which then still paid each doctor, hospital, and

other provider of health care more or less whatever they were billed,

with few questions asked. By contrast, for Medicare patients, the

Reagan administration had as early as 1983 imposed on the hospital

a centrally administered system of price controls that imposed a

common, uniform fee schedule for all hospitals in the entire nation.

(Were this essay not addressed to Princeton alumni, one might properly

call it a Soviet-style approach to hospital pricing). For his part,

President Bush followed suit by imposed a nationwide, centrally

set fee schedule similar with strict price controls on physicians

in early 1992, along with a total global budget for all annual Medicare

spending on physicians.

As a result of these tough price controls, Medicare spending per

beneficiary during most of the 1980s actually rose much less rapidly

than per-capita spending in the private sector. Indeed, private

insurers and the employers behind them loudly complained that the

annual premiums increases of 15% to 18% they suffered during the

late 1980s were in good part the result of a "cost shift"

from government to the private sector. The theory is that whenever

government tightly controls health spending, the providers of health

care simply increase the prices charged private payers or persuade

their patients to use added health services.

The onset of managed care

The rapid escalation of employer-paid insurance premiums, coming

as it did in the midst of the economics recession around 1990, set

the stage for the onset of what has come to be known "managed

care." At the core of this approach was the ability of private

employers, during the recession, to force upon their anxious employees

health insurance products that limited the employees’ choice

of providers to defined networks, which often limited direct access

to medical specialists, and which sometimes limited patients’

access to new and expensive medical technology — e.g., to new,

expensive brand-name medicines. Employees accepted these novel strictures

at the time, because they worried more about keeping their jobs

than about the design parameters of the health-insurance policy

that came with the job.

These limitations of choice enabled the health insurance companies

that were writing these policies to contract selectively with physicians,

hospitals, pharmacies, and other providers for the health care owed

the insured. Selective contracting, in turn, converted these providers

of health care into fiscally dependent subcontractors of particular

health plans. The plans could impose serious fiscal hardship on

individual providers, simply by canceling their contracts with the

plan. That fiscal dependence, and the constant economic threat it

implied, enabled the health plans to extract from the providers

of health care steep price discounts. It also enabled the health

plans to impose upon providers clinical practice guidelines that

determined whether or not a health plan would pay for particular

services rendered. Altogether, these novel relationships among insurance

plans, on the one hand, and the providers of health care and their

patients, on the other, constituted the phenomenon properly called

"managed care."

As is shown in Table 3, the attempt to control

American health spending through the techniques of "managed

care" did bend the time path of actual real per-capita health

spending during the period 1992-97 below the long-run spending trend

line. During the mid 1990s, real per-capita health spending rose

at rates much below the historical long-run average of 4.5%. The

health insurance premiums charged employers for their group policy

rose at ever smaller annual rates, reaching an average of a zero

increase in 1996. The percentage of GDP spent on health care was

virtually constant, hovering about 13.5%. In 1993 Congressional

Budget Office (CBO) had projected that health spending in the year

2000 would be $1.67 trillion, or close to 20% of the GDP. The actual

number for 2000 turned out to be $1.3 trillion, or only about 13%

of GDP.

Economic theory suggests that, in the tight labor markets of the

1990s, the bulk of these savings in health spending are likely to

have flown through to employees in the form of higher take-home

pay. That theory, however, is not widely shared among non-economists.

A more popular theory in the press, and especially among the providers

of health care, is that these savings reflect the denial of needed

care to the insured and that they flowed mainly into the bottom

line of employers and the paychecks of health insurance executives.

The "managed care" backlash unleashed by physicians, politicians,

and the media was driven by this popular theory.

Starting in 1997, with "managed care" in wholesale retreat,

overall average real per capita health spending in the U.S. has

been rising once again, at an ever-accelerating pace. As is seen

in Table 1, it now proceeds at roughly the

same high growth rate that was experienced during the late 1980s—albeit

still below the long-run historical trend line. For the 2001-2002

season, these increases are projected to be in the mid- to high

double digits, even for large employers, and in excess of 20% for

small employers and individuals.

Per capita health spending under the public Medicare and Medicaid

programs currently are still rising at much lower rates than those

in the private sector, partly as a result of cost-control measures

legislated in the late 1990s. It is only a matter of time until

these public programs must adapt to the prices and spending levels

set by the private sector. Furthermore, just as in the later 1980s,

private insurers and employers are convinced once again that the

tighter control of government health spending shifts costs to private

payers. Therefore, they will lobby the Congress to relax the reins

on public health spending. In short, the health-care cost crisis

of the late 1980s has returned to the U.S. in full bloom.

C. The next few Years in U.S. Health Policy

During the course of the past two decades, the legendary American

voter, has spoken clearly articulated the preferred health policy.

That legendary voter is worried about the cost of health care and

about losing health insurance coverage. Utterly convinced by TV

actors Harry and Louise that government ought not to introduce into

something as delicate as health care, however, the U.S. voter prefers

a private health insurance system. The voter does, of course, expect

private insurers to control the cost of health care, but not through

controls over the volume of health care, nor through downward pressure

on prices.

Volume controls represent "rationing," which is un-American,

at least insofar as insured Americans are concerned. Downward pressure

on the for prices hospital care is known to lead to nursing shortages

and hence reduce the quality of care. Downward pressure on physician

fees is known to detract from the quality of physician care, as

doctors are forced to defend their income by processing more patients

more quickly. Price controls of prescription drugs are known to

inhibit research and development by that industry.

In short, the American voter wants (1) instant access to (2) affordable

health care in a system that (3) controls health spending through

something other than prices or volume. To thoughtful persons, that

wish list poses a challenge. Indeed, to thoughtful persons, the

aspirations of the American voter in matters of health policy are

so young, to put it politely, that serious policy makers have long

despaired of taking voters’ aspirations seriously.

Health policy in this country therefore has been and is being forged

strictly among a narrow policy-making elite that could easily fit

into the Grand Ballroom of the Washington Hilton hotel. Within that

elite, there has been a decade-long, tenacious fight between two

distinct camps: the egalitarians, who would like to see health care

run on a social contract such as Canada’s, and the libertarians,

who view health care as a private consumption goods whose quantity

and quality can properly be rationed by the individual’s income.

During the debate over health reform in the early 1990s, for example,

Nobel Laureate economist Milton Friedman proposed the complete abolition

of the federal Medicare program for the elderly and the state-federal

Medicaid program for the poor. Instead, he advocated that families

have only catastrophic health insurance, with an up-front, out-of-pocket

deductible of $20,000 per year or 30% of the family’s income

during the last two years, whichever is lower (The Wall Street

Journal November 12, 1991). At the time of his writing, the

median pretax family income in the U.S. was $35,000, which means

that he had in mind a $10,500 deductible for such a family.

It appears that the libertarians are winning this contest. As national

health spending rises once again annually at double-digit rates,

the insurance industry is poised to segment its clientele more and

more by actuarial risk class, that is, by health status. It is achieved

through the process of computer-based "mass customization"

that allows insurers to tailor a family’s health insurance

policy ever more closely to its own "needs" — code

for "actuarial risk" or "health status." Many

of these new insurance products will be patterned on Milton Friedman’s

vision. Eventually, the Medicare program will move in this direction

as well. The net economic effect of these developments will be to

allocate less of the financial burden of health care to the chronically

healthy, who "consume" relatively little health care,

and more to the chronically sick, who "consume" relatively

more.

On the back of these trends, the health care system of the future

in the U.S. is likely to fall into at least four distinct tiers,

with the following offerings, by income class:

1. For the millions of uninsured who are unlikely to be covered

in this decade, if ever, under the emerging tight government budgets,

whatever they can afford with their budgets or can scrounge up as

health-care beggars from kindly doctors and hospitals.

2. For Medicaid beneficiaries and low-income employees in

firms that do offer employees health insurance, tightly managed

Health Maintenance Organizations (HMOs) that will seek to limit

choice and ration health care judiciously, in accordance with guidelines

and the premiums they are paid.

3. For middle- and upper income employees, mild if any rationing

and wider choice of provider and therapy under the so-called Preferred

Provider policies (PPOs) which will, however, charge higher premiums.

4. For very high-income people — executives prominent

among them — open ended indemnity policies without any limit

on choice and without any form of rationing—the perfect clientele

for boutique medicine.

There will of course be sundry tiers in between.

This is not a futuristic vision. The system is already in place,

albeit by happenstance and default. The difference will be an income-based

system will be more formally more formally and officially sanctioned

by the Congress and the state legislatures of the United States.

It would as yet remain politically incorrect to advocate such a

system explicitly.